How to Start a FinTech Company from Scratch

If you’re thinking about starting a fintech company, there has never been a more exciting time to build. Over the past decade, fintech has moved from being the “challenger” to becoming a central pillar of the global financial system.

The COVID-19 pandemic accelerated this shift dramatically. Suddenly, digital finance wasn’t just convenient; it became essential. People began to rely on mobile banking, digital payments, and app-based services as part of day-to-day life, and that behavior didn’t fade afterward.

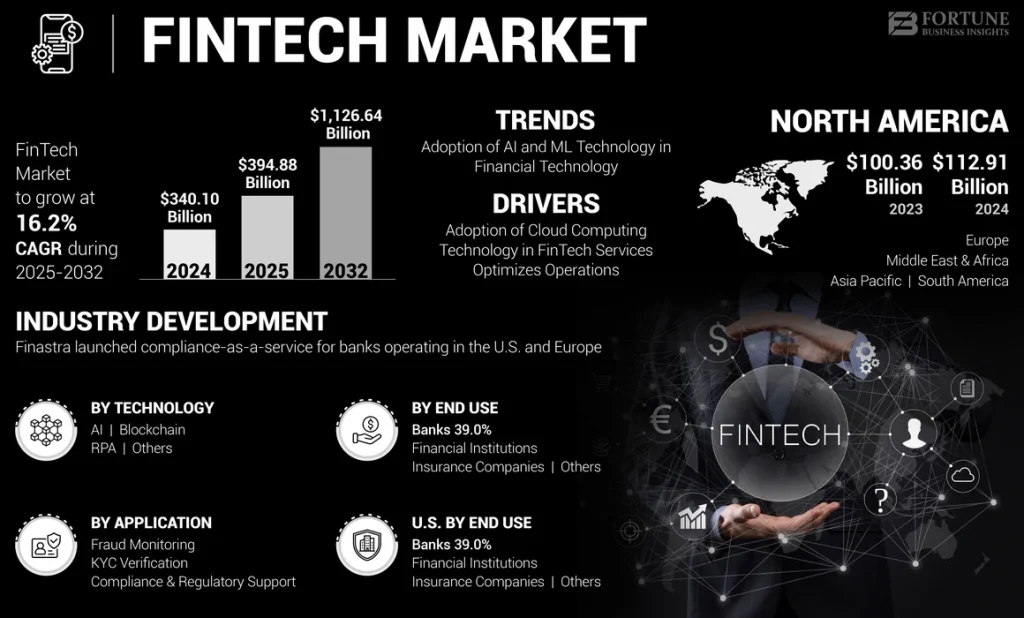

By 2032, fintech revenue is expected to hit $1.13 trillion. Today, users expect financial services to be fast, accessible, and entirely digital from the start.

This shift also opened new doors in emerging markets. Millions of people who were previously outside the formal financial system can now save, borrow, make payments, or grow their businesses using fintech platforms.

Mobile wallets, alternative credit scoring, micro-lending, and merchant payment apps are helping individuals and small enterprises access opportunities they never had before. The demand is real, the user base is expanding, and the market is far from saturated.

The challenge now is not whether fintech is needed, but building fintech solutions that are trustworthy, compliant, and culturally relevant.

Add to this the rise of open banking, where financial data can be securely shared to create new products, and the emergence of national digital identity systems and CBDCs, which make onboarding and digital payments smoother than ever.

Plus, many countries now offer regulatory sandboxes that allow fintech startups to test products legally with supervision. The barriers to experimenting have never been lower.

So, if you’re planning to build one, it’s the perfect time to learn how to start a FinTech company in an industry that’s evolving yet still full of opportunity. What fintech is and how to design for real-world use with today’s technology innovations hype. This blog will guide you through the steps.

What is FinTech?

FinTech, or Financial Technology, refers to the use of digital tools and software to handle financial activities. It allows these activities to happen online through apps and automated systems. For example, when someone uses a mobile app like Google Pay to send money directly from their bank account to another person’s account, they are using a FinTech service.

Source: https://www.nimbleappgenie.com/

Layers of the FinTech Value Chain

The FinTech ecosystem is made up of several interconnected layers that work together to deliver digital financial services. Each layer performs a specific function, from providing regulated financial infrastructure to designing user-friendly digital products.

Understanding these layers helps clarify how money moves across platforms and how everyday financial actions are enabled through technology.

#1 Banks and Licensed Financial Institutions

Banks form the core infrastructure of the financial system. They hold customer deposits, issue loans, maintain compliance with government regulations, and ensure financial stability.

Even when users engage through digital apps, the underlying money movement typically runs on banking rails. Without banks, FinTech services cannot facilitate financial regulated account management, lending, or transaction settlement.

#2 Payment Processors and Financial Networks

This layer manages the technical movement of money between accounts. Payment processors and card networks (such as Visa, Mastercard, and RuPay), along with digital payment infrastructures like UPI, route, authenticate, and settle transactions.

They ensure that payments are executed securely and reliably. These systems operate in the background, making digital payments appear instant and seamless to users.

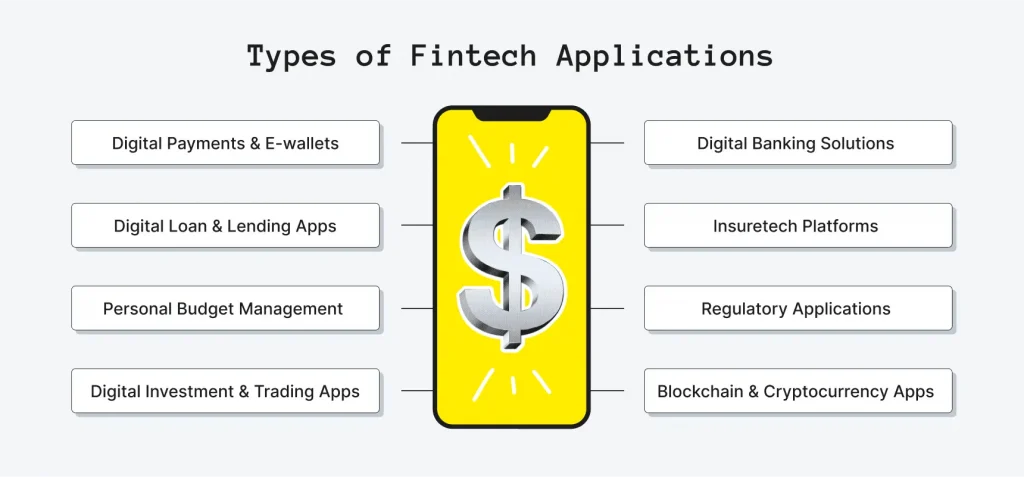

#3 FinTech Companies (Digital Platforms and Service Innovators)

FinTech companies build digital interfaces and financial applications that users interact with. They develop innovative fintech solutions such as:

- Mobile payment apps

- Online lending platforms

- Automated investment tools (robo-advisors)

- Digital insurance platforms

- Business financial dashboards and billing tools

Their focus is experience, accessibility, and speed, transforming traditional financial services into user-friendly digital products. While banks handle compliance and funds, FinTechs handle usability and innovation.

#4 End Users: Consumers and Businesses

This layer consists of individuals and companies that use FinTech services. Consumers may use apps to pay bills, send money, invest, save, or borrow. Businesses use FinTech tools to accept digital payments, manage accounts, or access working capital. Here are the types of fintech startups you need to know.

Steps to Build a Successful FinTech Company

Have an idea, where do I start? Here’s a simple guide to building a successful FinTech company step by step.

Step 1: Identify Your Target Users and the Problem to Solve

The first step in building a FinTech business is identifying a specific group of users who face financial challenges that existing tools can’t solve, a critical part of how to start a FinTech company that truly meets user needs.

These could be small business owners dealing with delayed invoice payments, freelancers managing irregular income and taxes, or first-time borrowers who lack traditional credit histories.

By understanding their daily financial workflow and the frustrations they repeatedly encounter, you ensure that your product has a clear purpose.

Studying existing apps and financial services also helps reveal what works, what doesn’t, and where meaningful gaps still exist. These gaps represent your opportunity to create a truly valuable solution.

Step 2: Define Your Value Proposition and Validate Market Demand

Once the gap is understood, the next step is to define your Unique Value Proposition (UVP), a clear, one-sentence explanation of why users should choose your fintech solution over others. This could be faster transactions, lower fees, easier onboarding, or a better personalized experience.

Before moving into development, it is crucial to validate whether people genuinely want your solution. This can be done through simple landing pages, waitlist sign-ups, small prototype demos, or user feedback surveys.

If potential users show real interest by registering, requesting access, or agreeing to test, you gain confirmation that the concept has practical demand. Validation ensures you build something people will actually use, not just something that sounds promising in theory.

Step 3: Define the Minimum Viable Product (MVP)

The first step in developing a FinTech product is defining the Minimum Viable Product. This means focusing only on the core features required to solve the user’s primary problem, rather than trying to build a fully polished platform from the start.

In most FinTech products, the MVP includes secure login and identity verification (KYC), a simple dashboard where users can view their financial activities, one core function such as sending money, borrowing, investing, or expense tracking, and basic customer support with fraud prevention systems.

Prioritizing these essentials allows the product to launch quickly, test real user behavior, and gather feedback early without unnecessary complexity.

Step 4: Choose the Right FinTech Business Models

FinTech companies operate through different business models depending on their target audience and delivery approach.

In the B2C (Business-to-Consumer) model, the company provides financial services directly to individual users through digital banking platforms. This model helps entrepreneurs build a strong user base and brand presence while focusing on customer experience, personalization, and trust.

In the B2B (Business-to-Business) model, FinTechs offer financial tools, infrastructure, or software solutions to other companies. This allows entrepreneurs to tap into stable, long-term business relationships, generate recurring revenue, and scale efficiently by solving operational or financial challenges for organizations.

The B2B2C (Business-to-Business-to-Consumer) model combines both approaches. A FinTech partners with another business to deliver services to end consumers, while the partner handles customer-facing interactions. For entrepreneurs, this model reduces customer acquisition costs and enables rapid expansion, since the FinTech leverages the partner’s brand and user base.

Source: https://www.upsilonit.com/

Each model provides unique advantages. The choice depends on how the entrepreneur plans to create value, build trust, and scale sustainably in the financial ecosystem.

Step 5: Choose the Right Technology Stack

Once the MVP scope is clear, the next step is selecting the technology stack that will power the platform.

For the backend, many FinTech teams choose languages like Node.js, Go, or Java due to their high performance and reliability.

On the frontend, frameworks such as React or Flutter are commonly used to build responsive web and mobile interfaces.

Databases like PostgreSQL or MongoDB store financial data securely, while cloud services such as AWS, Azure, or Google Cloud provide hosting and scalability.

Throughout the system, strong security measures are critical to ensure user trust. The tech stack determines the system’s speed, scalability, and safety from day one.

Step 6: Building the Product

The final step is building the product, and this is where a skilled development team makes the real difference. FinTech companies typically choose between two paths — building from scratch or leveraging ready-made solutions and Banking-as-a-Service (BaaS) providers.

An experienced development team can identify which parts of the system should be custom-built for a competitive edge and which can rely on existing financial infrastructure. By combining in-house expertise with trusted BaaS integrations, teams can launch faster, ensure compliance, and maintain flexibility for future scaling.

In most successful FinTech projects, it’s the development team’s balance of custom engineering and smart integration that turns a concept into a reliable, scalable product.

Step 7: Launch, Test, and Continuously Improve

Once your FinTech product is ready, launch it first to a small group of targeted early users rather than a wide audience. This controlled rollout helps you understand how people actually use the product in real situations, revealing which features deliver real value and where friction still exists.

Track user behavior closely, observe what they do, not just what they say, and use this feedback to refine user flows, enhance performance, and fix any barriers that slow adoption. As the experience becomes smoother and trust builds within this initial user base, gradually expand to a larger audience.

Choosing Your Product Direction

When building a FinTech solution, one of the most important early decisions is defining what role your product will play in a user’s financial life. Broadly, FinTech products evolve in three possible directions:

A. Becoming the User’s Primary Banking Relationship

In this approach, your product aims to become the customer’s main financial account, the place where salaries are deposited, everyday payments are made, and savings are stored. This model requires strong trust, a reliable mobile banking app experience, and smooth onboarding.

Users should feel confident enough to make your platform the first place they go for managing money.

Examples of features typically included are debit cards, digital wallets, UPI payments, and daily transaction tools. The long-term goal is to make your product part of the user’s everyday financial routine.

B. Building a Point-Based FinTech Solution (Solving One Core Problem)

Instead of trying to replace a bank, some FinTech products focus on one very specific financial pain point and solve it exceptionally well. This helps avoid complexity and allows rapid user adoption.

For example, a platform may only handle bill payments, automate savings based on spending habits, or offer smart credit scoring and lending tools.

By focusing on one core feature, the product becomes easier to develop, test, market, and scale. Users choose it because it is the best at that one thing.

C. Creating Financial Infrastructure (Tools for Other FinTech Companies)

Another direction is to build infrastructure rather than consumer-facing products. Here, your customers are not individuals but other FinTech startups, banks, or digital platforms.

Your product provides the building blocks they need, such as identity verification (KYC) APIs, payout systems, card issuing services, or credit scoring engines.

This model can be highly scalable because once the infrastructure is built, multiple companies can integrate it. The focus is on reliability, compliance, and strong developer experience.

Integration Points in the FinTech Ecosystem

FinTech comes in wherever money meets technology. It’s not here to replace banks or traditional finance. Instead, it makes financial tasks smoother, quicker, and more naturally blended into the digital tools we already use. Here’s where you’ll notice it the most.

1. Payments: Making Transactions Feel Effortless

Think about paying through a QR code at a shop, adding items to an online cart, or sending money to a friend in seconds. That’s FinTech at work. These platforms sit quietly behind the scenes, connecting customers, merchants, banks, and card networks so the payment just… happens. No hassle, no waiting.

2. Lending: Faster Decisions Without the Paper Chase

Getting a loan used to mean forms, bank visits, and waiting. Today, FinTech platforms use data and automated checks to understand credit behavior in minutes. This is how we get instant debt consolidation loans, quick business credit, and Buy Now Pay Later options right at checkout. The idea is simple: smarter decisions, less paperwork.

3. Wealth Management: Investing That Doesn’t Feel Intimidating

Mobile investment apps and digital advisory platforms have made investing feel more approachable. They help users track portfolios, set goals, and understand where their money is going. Established platforms like Vector Vest take this further by offering automated stock ratings and advisory signals for both beginner and experienced investors.

Even someone investing for the first time can get guidance without needing to be an expert or meet a financial advisor in person.

4. Embedded Finance: When Finance Lives Inside Other Apps

You’ve probably noticed this without realizing it. You order food or shop online, and the app lets you store a balance, pay instantly, or even access quick credit. That’s embedded finance. Instead of jumping between apps, the financial part just blends into the experience you’re already in.

Source: https://broscorp.net/

5. Insurance: Simple, Digital, and No Agents Required

Insurance has shifted online, too. Comparing policies, verifying details, and filing claims can often be done through guided screens. No paperwork. No repeating information. No waiting in long queues or coordinating with agents unless you want to.

FinTech doesn’t replace traditional finance. It enhances it by embedding financial services directly into digital environments, making everyday financial interactions smoother and more convenient.

Navigating the Regulatory and Compliance Landscape in FinTech

Starting a FinTech startup isn’t just about technology and customers; it’s also about building a business that regulators, banks, and users trust. Think of compliance as the safety rails on your journey:

Choosing Your Jurisdiction and Licensing Strategy

Every country has different financial regulations, licensing requirements, and operational rules. Choosing the right jurisdiction is one of the first critical decisions for a FinTech startup.

Jurisdiction Matters: Some countries offer fintech-friendly regulatory sandboxes, faster licensing, and lower capital requirements, while others have stricter rules.

Licensing Pathways

Different FinTech models require specific licenses depending on the services offered:

EMI (Electronic Money Institution): For digital wallets or stored-value accounts.

MSB (Money Services Business): For remittances, currency exchange, and money transfer services.

Lending Licenses / NBFC: For platforms offering loans or credit.

Broker Licenses: For investment advisory or securities trading platforms.

Selecting the correct license early ensures compliance and smooth operational scaling.

AML & KYC Workflow Levels

Anti-Money Laundering (AML) and Know Your Customer (KYC) measures are tiered by risk:

KYC Lite: Basic identity verification for low-risk accounts.

Full KYC: Detailed identity checks for higher-risk or higher-value accounts.

KYB (Know Your Business): Corporate verification, including ownership structure, financial health, and regulatory checks.

Effective workflows reduce fraud risk and satisfy regulatory requirements.

PCI DSS Compliance

Startups handling payment card data must comply with PCI DSS standards, ensuring secure transactions and safeguarding users’ financial information.

Data Residency & Localization

Some jurisdictions require that financial and personal data remain stored locally. Compliance with data protection residency and privacy laws (e.g., GDPR, PDPA) is essential to avoid legal penalties and maintain customer trust.

Consumer Dispute Redressal & Chargebacks

Regulations often mandate clear processes for resolving consumer complaints and chargebacks. Transparent and efficient systems protect users while minimizing financial and reputational risk.

Transaction Monitoring Rules

Real-time monitoring of transactions helps detect suspicious or unusual activities, such as fraudulent transfers or money laundering attempts. Automated alerts and reporting systems are crucial for regulatory compliance and fraud prevention.

To manage outstanding payments efficiently, debt collection software is used to track overdue accounts and maintain accurate works.

Security & Fraud Prevention Systems: How FinTechs Protect Users

In financial technology, security isn’t just a feature; it’s the backbone of trust. Users expect their money and data to be safe, and even a small breach can damage credibility irreversibly. Seed-stage startups implement several key security and fraud prevention systems:

1. Device Fingerprinting

This technology identifies the devices your users log in from, helping detect unusual devices or locations. It’s one of the first lines of defense against account takeovers.

Source: https://www.techmagic.co/

2. Transaction Anomaly Detection

Every transaction is monitored in real time. Systems flag unusual patterns, such as sudden large transfers or repeated failed payments, so suspicious activity can be reviewed immediately.

3. Behavioral Analytics

Beyond simple rules, behavioral analytics looks at how users interact with your platform—typing speed, navigation patterns, and login times to detect potential fraud before it escalates.

4. Chargeback Defense Systems

Disputed payments (chargebacks) are a common source of losses. Automated verification, documentation, and fraud scoring help reduce these financial companies’ risks.

5. Blockchain-Based Audit Trails

Blockchain creates permanent, tamper-proof records of transactions. This ensures transparency, simplifies audits, and strengthens regulatory compliance.

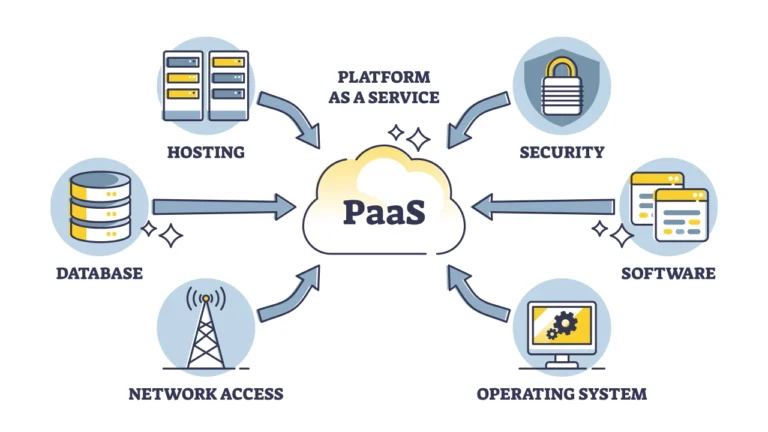

How Platform-as-a-Service Can Accelerate Your FinTech Startup

For many FinTech founders, building the technology infrastructure from scratch can be daunting, expensive, and time-consuming. This is where Platform-as-a-Service (PaaS) comes in as a solution.

Think of it as renting a ready-to-drive car instead of manufacturing one yourself. You get to focus on the journey instead of the engineering. The same approach applies when figuring out how to start a FinTech company the smart way.

When to Choose PaaS Over Building Infrastructure

Choosing PaaS is particularly advantageous when:

- You want to launch quickly without spending months on backend development.

- Your venture capital is limited, and building infrastructure from scratch would be cost-prohibitive.

- You need built-in compliance, security protocols, and scalability from day one.

- You want to test market demand before committing to long-term infrastructure investments.

While startups with unique, highly differentiated tech innovations may eventually build their own systems, PaaS allows most early-stage fintech companies to get to market faster and safer.

Benefits of PaaS

- #1 Lower Upfront Cost: You avoid the massive initial investment required for servers, software licenses, and custom development.

- #2 Faster Launch: Pre-built modules enable quicker integration, reducing time-to-market from months to weeks.

- #3 Built-In Compliance: PaaS providers often offer KYC/AML, PCI-DSS, and other regulatory tools integrated into the platform.

- #4 Scalable Infrastructure: As your user base grows, the platform can scale seamlessly without additional heavy investment.

Source: https://63sats.com/blog/

Risks to Consider

While PaaS offers many advantages, startups should recognize the value of having a capable development team behind the product.

Provider Dependency: Relying entirely on a PaaS provider can limit flexibility and control. A strong development team can build independent layers, manage integrations, and ensure the product continues to function even if the provider changes terms or services.

Fee Structure Complexity: Many PaaS platforms charge per user or transaction, which can increase costs as you scale. A skilled development team can design cost-efficient architectures, optimize resource usage, and plan for long-term scalability without being locked into one pricing model.

In short, a good development team turns PaaS from a dependency into an advantage, using it strategically rather than relying on it completely.

Future Opportunities & Investment Hotspots

The FinTech landscape continues to evolve rapidly. Emerging areas to watch include:

1. AI-Native Underwriting Systems

Lending is shifting away from old credit score models. New AI-driven underwriting looks at spending behavior, payment patterns, and real-time transaction data to understand someone’s financial reliability. This makes credit decisions quicker, fairer, and more accessible for people who may not have a traditional credit history.

2. SME-Focused Financial Operating Systems

Small businesses often juggle accounting, payments, payroll, and taxes across multiple tools. FinTech platforms that bring these functions into one unified dashboard can save business owners time, reduce errors, and simplify operations. It’s not just software; it becomes part of how the business runs day-to-day.

3. Tokenization of Real-World Assets

Assets like real estate or infrastructure are usually expensive and hard to trade. Tokenization breaks them into smaller digital units so more people can invest, and owners can unlock liquidity. In simple terms, it turns big, slow-moving assets into accessible, digital investment opportunities.

4. Carbon Accounting and Green Finance

Sustainability is becoming a business requirement, not just an ethical choice. FinTech is stepping in to help companies measure their carbon footprint, buy carbon credits, or access incentives for eco-friendly work. This makes environmental responsibility easier to track, verify, and reward.

5. Payroll-Powered Lending and Salary-Linked Products

Instead of evaluating borrowers purely on financial statements, some FinTechs are linking credit to income flows. When loans are tied to salary deposits or payroll systems, repayment becomes predictable, and risk goes down. This opens a stable, affordable credit path for employees who may struggle with traditional loans. Once these loans are funded, they need efficient servicing systems to manage repayments. Loan servicing platforms like Bryt Software automate payment tracking and borrower communications, keeping these alternative lending products running smoothly.

Targeting these emerging trends can position startups at the forefront of innovation and attract investor interest.

Performance Metrics & KPIs

Tracking the right metrics is crucial for FinTech startups to understand growth, user behavior, and operational efficiency. At this stage, FP&A software plays a critical role by enabling teams to forecast performance, model scenarios, and align financial planning with real-time business data. Key performance indicators (KPIs) help founders make data-driven decisions and demonstrate credibility to potential investors.

Activation Rate

Measures how many users actually use your core financial service feature (e.g., sending a payment, applying for a loan). A high activation rate indicates your product is delivering real value.

Retention Cohorts

Tracks long-term user engagement over time. Understanding retention helps identify whether your product achieves product-market fit and keeps current customers coming back. Cohort analysis helps identify retention patterns and user behavior trends, enabling fintech companies to improve customer engagement and optimize long-term retention strategies.

CAC: LTV Ratio

The ratio of Customer Acquisition Cost (CAC) to Customer Lifetime Value (LTV) measures growth sustainability. A lower ratio indicates more efficient growth and better return on marketing investment.

Gross Transaction Volume (GTV)

Represents the total monetary value processed on your platform. This is a core metric for scaling and demonstrating traction to investors.

Average Revenue Per User (ARPU)

Shows how effectively your platform monetizes its user base. Increasing ARPU signals stronger revenue generation per customer.

Fraud-to-Volume Ratio

Measures the proportion of fraudulent transactions relative to total transaction volume. A low ratio indicates effective risk management and fraud prevention systems.

Partner with Appkodes

If you’re exploring how to start a fintech company, partnering with Appkodes, a leading startup mobile app development company, can simplify your build decisions. Many founders begin with ideas around investment apps for beginners, evolving into PFM features and eventually into broader personal finance tools.

These fall under personal financial management tools, where clarity, trust, and frictionless user experience are essential.

When building a fintech startup mobile app, your team will move through the app development process step-by-step: concept validation, feature scoping, UI/UX design development, launch, and compliance updates.

Instead of figuring out everything alone, Appkodes helps you structure what features are needed at each stage so you don’t overload the first version.

Leveraging no code MVP development, you can quickly validate ideas and build a functional prototype without heavy coding, saving time and resources.

Choosing software development languages is another key layer. For backend logic, secure, scalable stacks are common.

This leads directly into backend infrastructure, which must handle encrypted data storage, stable transaction processing, banking API or payment gateway integrations, and a scalable architecture ready for growth.

By working with Appkodes, you don’t just get code written; you get guidance on the structure that supports compliance, trust, and user growth from day one, making your fintech startup launch smoother and more reliable.

Frequently Asked Questions

Q1. What’s the real difference between Challenger Banks and Neobanks?

A Challenger Bank holds its own license and operates like a full bank. A Neobank focuses on digital experience and partners with licensed banks. For a founder, this choice decides your compliance load, launch speed, and trust model.

Q2. Why should founders research competitors before entering the financial market?

Understanding the financial market and competitor apps shows where users are still frustrated. This helps you build a solution that feels user-centric, not just another fintech application with similar features.

Q3. How can a financial app retain existing customers long-term?

Retention comes from everyday usefulness: personalized insights, transparent fees, and friction-free support. When users feel understood, your financial app becomes part of their routine, not something they open only in emergencies.

Q4. Should my fintech app support digital currencies?

Supporting digital currencies can expand your audience, but only if your users value it. Think user-first: does crypto simplify their life or complicate it? Add features only when they improve real financial outcomes.

Q5. How do fintech applications securely process financial transactions?

Ensure every transaction passes through KYC, encrypted data layers, banking API checks, and fraud monitoring. A secure system builds confidence and lets users trust your app with their money, not just try it.

Arun Andiselvam

Founder of AppKodes. As a serial entrepreneur, I have successfully established five brands over the past 12 years. After creating a successful rank tracker for SEO agencies, I am currently dedicated to developing the world's first SEO Project Management software.